Tony Swicer is the president of the Palm Beach Coin Club, the vice president of Florida United Numismatists (FUN), and an avid collector of Kentucky bank notes. In this interview, he discusses the history of the regional banking system of the 19th and 20th centuries, the thrill of collecting his home-state notes, and the advantages of collecting currency over coins. Tony can be reached via FUN.

I started collecting when I was about 10 years old. My father was in the Air Force, so he got me started collecting everything—coins, stamps, military insignias, baseball cards, all kinds of stuff. I settled on coins, maybe because they’re worth the most money. I don’t know why particularly, but I just did. I collected coins from probably 1959 to the late ’70s when I sold my collection. I collected dollar-size metals for 10 years, and I sold that collection in about 1990.

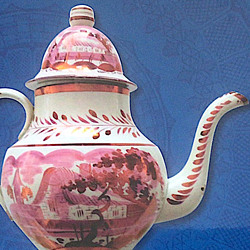

An 1882 series $5 note from Louisville, Kentucky. Grade: Superb Gem Uncirculated.

Then I floundered around for several years, not knowing what I wanted to collect. But I was still in the coin business, buying and selling, when it hit me: Why not collect my home-state notes? They’re very rare, and in the long run they’d probably appreciate.

The bank notes I collect date from 1863 through 1935. I bought the Don C. Kelly book, and it told me about all the banks, the number of known notes for each bank, and the pricing. Basically, you have to go out and buy them. You can’t find them anymore because the federal government recalled them all in 1935, and most of them have been turned in. There are about 600,000 known notes of all types in the United States, from every state.

When you consider that there were 12,635 chartered banks, 600,000 is not a lot of notes. That’s just fifty per bank on average. That’s how rare they are.

“For a while, California had its own nationals, what they called gold bank notes.”

I started collecting notes from Kentucky because it was my home state. It’s a thrill to get a note with the name of your city on it, too. When I acquired a bank note from my hometown bank that sold me a car, that was really exciting. Right now I’ve got about 15 notes from my hometown. The last note I bought was the only one if its kind known—an 1875 large-size note—and I thought if I don’t buy it now I’ll never see it again in my lifetime, so I bought it for $3,000. It was a bargain.

After I started collecting, I visited most of these towns. A lot of times the banks are long gone, but you can visualize in your mind what the place looked like.

I started buying bank notes at local coin shows, then bigger shows, and then I started buying them at national auctions because they were more plentiful. I bought 15 in one auction out in Beverly Hills a couple years ago.

I’ve been doing this for six years and I have about 215 different bank notes from Kentucky. It’s the thrill of the hunt that excites me. I hope to get over 400 before I’m done, maybe in another 10 years, if I’m lucky, and then maybe I’ll put them all up at auction.

Collectors Weekly: What are some of the shows you attend?

Swicer: I went to the ANA show in Los Angeles in 2009. I go to the FUN Convention every year in Orlando because it’s only two-and-a-half hours away. And I’ve been to the Cincinnati show. I used to do the national circuit in the 1980s, but I’ve cut way back with the recession and everything.

This 1875 series note from Newport, Kentucky is the only known $5 note from this bank.

These days, I mainly get my notes from national auction companies like Heritage, Stack’s, and Goldberg’s. I just go online and bid.

I bought those 15 Kentucky notes I mentioned at a Goldberg auction in Beverly Hills, online. And that’s how I’ve been acquiring them, just one here, one there. If I get one or two a month, I’m happy. Even locally I’ve picked up a couple of rarities, like a serial number one from Owensboro, Kentucky down at the Fort Lauderdale monthly coin show. It’s just incredible to find a serial number one. I snatched that up right away.

As I said, the average number of notes is fifty per bank, so they’re very rare. They made 5-dollar bills, tens, and twenties. Some of the bigger banks made fifties and hundreds. There are hoards that come out periodically. In Lexington, Kentucky, one bank had about 500 preserved notes, and I got some those in choice uncirculated condition.

Collectors Weekly: Do people collect by state?

Swicer: Yes. Even a lot of dealers collect by state. For example, Littleton Coin Company up in New Hampshire is mainly a mail-order company that’s been around since 1946. Littleton’s owner collects New Hampshire—he’s got about 250 different bank notes from the state. A lot of people also collect by condition. But most people, I believe, collect by state.

")

A 1902 series Owensboro $5 note, labeled serial #1 (bottom left).

Condition is not that critical. The Kelly book is for pricing in fine condition, which is mediocre at best. You don’t find a lot of these notes much nicer than that. I do have some uncirculated notes, but they’re few and far between. To find them uncirculated is really tough. So condition’s not that important, but in the Kelly book, for every grade you go up, you add 25 percent to the value. The grading scales are ‘fine’, ‘very fine’, ‘extremely fine’, ‘about uncirculated’, then ‘uncirculated’.

If someone finds a hoard of old bank notes, a lot of times they will uncover a few uncirculated notes, but for many banks there are simply no uncirculated notes available. A lot of times the best known note might be an extremely fine, which means maybe two or three creases and pretty crisp, but not new. So anything fine or better is collectible in national bank notes.

Collectors Weekly: Where was the first note issued in Kentucky?

Swicer: I believe in Louisville, and the last note in the whole country was also issued in Louisville, which is just a coincidence. The first national bank note in the United States was for the First National Bank of Philadelphia, and it got charter number one. That’s on all of its notes. Each bank had its own charter number, and every 20 years the charter was renewable.

Collectors Weekly: When did the first bank in Kentucky open?

Swicer: I believe it was probably First National Bank in Louisville, chartered in 1863. That’s when it all started, and that was charter number 109.

At the time, Kentucky had 111 towns, and a total of 238 banks were issued charters. My hometown, Newport, Kentucky, had three different banks over the years, each with a different charter number.

Collectors Weekly: Where were Kentucky’s biggest banks?

Swicer: Louisville and Lexington probably had the biggest, most prosperous banks, which means they printed a lot more notes. Those notes are more common today than the notes from the small-city banks. Louisville had 12 to 15 chartered banks, while my hometown, right across the river from Cincinnati, Ohio, had three.

Some banks were named after the person who started the bank, like the Joe Black Bank of Louisville. Others were just the First National Bank of Podunk, or whatever. A lot of the Kentucky notes were from German National Bank. They changed that name after World War I.

Collectors Weekly: Could Kentucky notes be used in a different state?

Swicer: That was the nice thing about it. They were printed by the Federal Reserve, so they could be used anywhere in the United States. National bank notes, even ones printed for chartered banks, were accepted all over the country with no problem. The notes that had been printed before that were regional. If you went far enough away from a given bank, they wouldn’t accept the notes. As a result, a lot of notes were traded at a discount.

Collectors Weekly: How did merchants make change?

Swicer: Well, at first everybody wanted hard coinage, silver and gold. After a period of time, though, they began to accept the notes. California actually wanted its notes to be redeemable in gold, and for a while they had their own nationals, what they called gold bank notes. But after 10 years they used the regular national bank notes like everybody else. Over time, merchants and customers alike began to accept the notes and realized that it was just as good as coinage. They were forced to. Either you took it or you didn’t get paid.

Collectors Weekly: How did a bank get chartered?

Swicer: Each bank came up with a minimum of $25,000, which they’d give to the government. That money would be put in government bonds, drawing interest. In turn, the bank would get currency printed by the Bureau of Engraving and Printing, the BEP.

Each bank was issued notes with its name, city, and state on it. In the beginning the notes had to be hand signed by the cashier and the president of the bank, so a lot of times those signatures were forged. The signature authorized the notes and made them legal tender through that bank. Finally, I believe in the early 1900s, the BEP started printing signatures on the notes.

A 1902 series $20 note from Hodgenville, Kentucky, Abraham Lincoln’s birthplace.

See, the government would make these sheets of notes, but they wouldn’t print the whole thing. A five-dollar bill would have Lincoln on it, a ten would have Hamilton, etcetera. They would all have the same denomination and vignettes on them. Then they’d put the name of the bank and the charter number and all that on it. So they had a bunch of sheets already made up, half printed, and then when a new bank came online, they’d add in the new bank’s information.

The notes were standardized. Each $5 note had the same vignette, each $10 note had the same vignette, and so on. But they changed the series periodically, and that would give the currency a whole new look. In 1863 the notes looked one way. In 1875, they changed the notes and they all looked different. Notes from 1902 changed again, and then in 1929, of course, they went to the small-sized notes that we use today. Before that, all notes were larger.

The 1929 series, for example, is very plain looking, with no real vignettes on the front, just the printing of the bank and the serial numbers and all that stuff. The older notes had more vignettes on them, featuring people and different figures.

Collectors Weekly: Did the Federal Reserve print its own notes, too?

Swicer: Yes, they started printing paper money in 1861. This whole national bank note system came about because of the Civil War. They needed extra money to pay for the Union war effort. Making paper money was a way for the government to get more money into its coffers. They issued bonds against it so that the banks had something to back up their money.

At the same time, the government was issuing Federal Reserve notes, which were mostly backed by silver and gold until the mid-’20s. Since the 1930s, Federal Reserve notes have not been backed by anything.

Before the national bank note system there were several financial panics, one from 1835 to 1837 and another in the 1850s. Back then, banks just issued their own notes with nothing to back them up, and they all went bankrupt. Those notes are known as broken bank notes or obsoletes. They were outlawed after the Civil War when the government started issuing notes.

Collectors Weekly: The colonists also used paper money, right?

Swicer: Colonial currency was used to pay for the Revolutionary War. That was the main reason they came up with it. Early in the history of the country we did not have any gold coins, so people had to use paper, or they bartered. The early gold strikes in the United States were in 1829, and the government started coining after that. We used foreign coinage until 1857 because we had such a shortage of coins, especially silver and gold. Copper was easier to get—we bought copper from England for years after the Revolutionary War. But we didn’t have coinage of any consequence until the mid-1850s.

Collectors Weekly: What was the smallest denomination of paper money?

Swicer: From 1863 until 1875 we had fractional currency. They made three-, five-, 10-, 15-, 25-, and 50-cent notes because coins were being hoarded during the Civil War. In terms of the bank notes, the first year they made one-, two- and five-dollar notes was 1863. Around 1900, though, the smallest denomination was a five. The denominations went all the way up to 1,000, but they discontinued those pretty quick. After the turn of the century, a 100-dollar bill was pretty much the highest. The higher the denomination, the fewer they made, so they’re pretty scarce. I do have some three-hundreds in my collection, but they are very rare—they cost a couple thousand dollars each.

Collectors Weekly: What are some of your favorite bank notes in your collection?

Swicer: I’ve got an 1882 note from Louisville that’s in absolutely perfect condition—it has no signs of wear whatsoever. I really like my serial number one from Owensboro, Kentucky, 1902, because they started with number one and numbered them right on out through however many notes they made. And of course I get a kick out of having notes from my hometown banks. Those are my favorites, I guess. But generally, to have an older note in choice, uncirculated condition is amazing. I’ve got one from Hodgenville, Kentucky, where Abraham Lincoln was born, in choice uncirculated condition.

Collectors Weekly: How do you store your notes?

Swicer: They’re all in hard, clear currency holders. There’s no PVC on them, and I keep them in a safety deposit box at the bank. Periodically I look at them. I keep a list on my computer of what I have. That way, I can update it every time I buy a new note.

Once I get a complete collection of my hometown bank notes, I’m going to put them on a disc and send them to the local library so they have a copy of everything I’ve got because I don’t think they have more than one or two notes.

Collectors Weekly: Is there anything else that you want to say about collecting bank notes?

Swicer: To me, collecting bank notes is just a general progression. When you’re a coin collector, you go from coins to maybe metals. A lot of us go that way. We start out with coins, and then we go on to other things. Eventually some of us get into paper money—that’s how it happened with me. I just narrowed it down to bank notes. Grading is not as important on bank notes as it is on coins, and the really nice thing about bank notes is they’re lightweight. You can lug your whole collection in a briefcase. In coinage, you can’t do that. They’re just too heavy. Paper money is much easier to store and handle.

(All images in this article courtesy Tony Swicer, vice president of FUN)

John Hotchner Exposes Philatelic Errors, Freaks, and Oddities

John Hotchner Exposes Philatelic Errors, Freaks, and Oddities

An Interview with Smithsonian Coin and Currency Curator Richard Doty

An Interview with Smithsonian Coin and Currency Curator Richard Doty John Hotchner Exposes Philatelic Errors, Freaks, and Oddities

John Hotchner Exposes Philatelic Errors, Freaks, and Oddities Taking Stock of Scripophily

Taking Stock of Scripophily Colonial and Continental CurrencyUntil the Massachusetts Bay Colony issued the first paper currency in 1690,…

Colonial and Continental CurrencyUntil the Massachusetts Bay Colony issued the first paper currency in 1690,… US Paper MoneyCollectors of U.S. paper money have a rich array of notes and certificates …

US Paper MoneyCollectors of U.S. paper money have a rich array of notes and certificates … Mari Tepper: Laying it on the Line

Mari Tepper: Laying it on the Line Nice Ice: Valerie Hammond on the Genteel Charm of Vintage Canadian Costume Jewelry

Nice Ice: Valerie Hammond on the Genteel Charm of Vintage Canadian Costume Jewelry How Jim Heimann Got Crazy for California Architecture

How Jim Heimann Got Crazy for California Architecture Modernist Man: Jock Peters May Be the Most Influential Architect You've Never Heard Of

Modernist Man: Jock Peters May Be the Most Influential Architect You've Never Heard Of Meet Cute: Were Kokeshi Dolls the Models for Hello Kitty, Pokemon, and Be@rbrick?

Meet Cute: Were Kokeshi Dolls the Models for Hello Kitty, Pokemon, and Be@rbrick? When the King of Comedy Posters Set His Surreal Sights on the World of Rock 'n' Roll

When the King of Comedy Posters Set His Surreal Sights on the World of Rock 'n' Roll How One Artist Makes New Art From Old Coloring Books and Found Photos

How One Artist Makes New Art From Old Coloring Books and Found Photos Say Cheese! How Bad Photography Has Changed Our Definition of Good Pictures

Say Cheese! How Bad Photography Has Changed Our Definition of Good Pictures Middle Earthenware: One Family's Quest to Reclaim Its Place in British Pottery History

Middle Earthenware: One Family's Quest to Reclaim Its Place in British Pottery History Fancy Fowl: How an Evil Sea Captain and a Beloved Queen Made the World Crave KFC

Fancy Fowl: How an Evil Sea Captain and a Beloved Queen Made the World Crave KFC

I saw 3 bills, all i believe to be from 1929. A Campbellsville $10, a Lebanon $10, and a Campbellsville $20 serial number 2. What would those cost?

Campbellsville $10 in Fine condition lists for $200 in the Kelley book. The $20 #2 should be worth at least $400. The Lebanon charter 3988 is about $125 in Fine. Charter #4271 is $250, and Charter #2150 is $150.

I need a $5 type 1 Ky. Bank note. Would like one from Louisville charter # 109

I’m not seeing any for sale anywhere

Where’s a good place to search for Ky. Bank Notes